Creating A New Unsecured Loan

An unsecured loan is a loan that doesn't require any type of collateral. Instead of relying on a borrower's assets as security, financial institutions approve unsecured loans based on a borrower’s creditworthiness.

Before creating a unsecured term loan contract, make sure that:

-

the customer is recorded in Core Banking,

-

a settlement account (a current account contract for the same customer) is set up for the desired currency,

-

and the limits are configured according to Core Banking's setup.

-

Open the Contracts page as described in the Managing Contracts section.

-

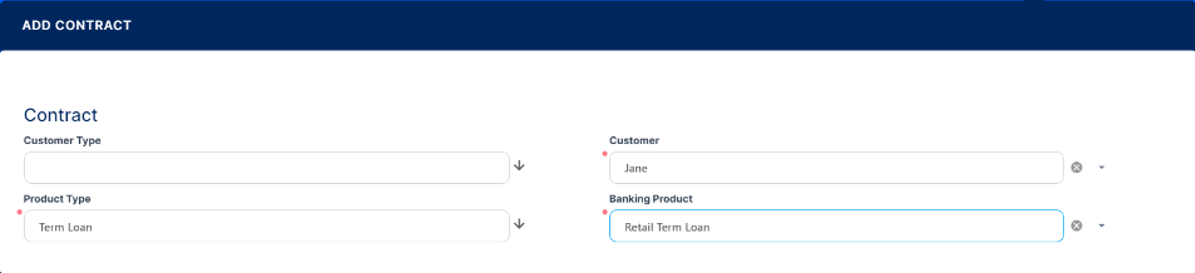

Click the Insert button to display the Add Contract page, the initial page when you insert any type of contract.

-

Fill in the following fields:

-

Customer Type - Optionally, select the type of the customer for the contract, to filter the displayed customers in the next field.

-

Customer - Select from the list the customer for whom you are creating a contract.

-

Product Type - Select from the list the product type to filter the list of banking products accordingly.

-

Banking Product - Select from the list the desired banking product.

Be careful when choosing the values for the previously mentioned fields because you can't modify them after saving the contract!

Make sure that you select

Term Loan in the Product Type field and an Unsecured Loan banking product in the Banking Product field.-

Click the Save and Reload button.

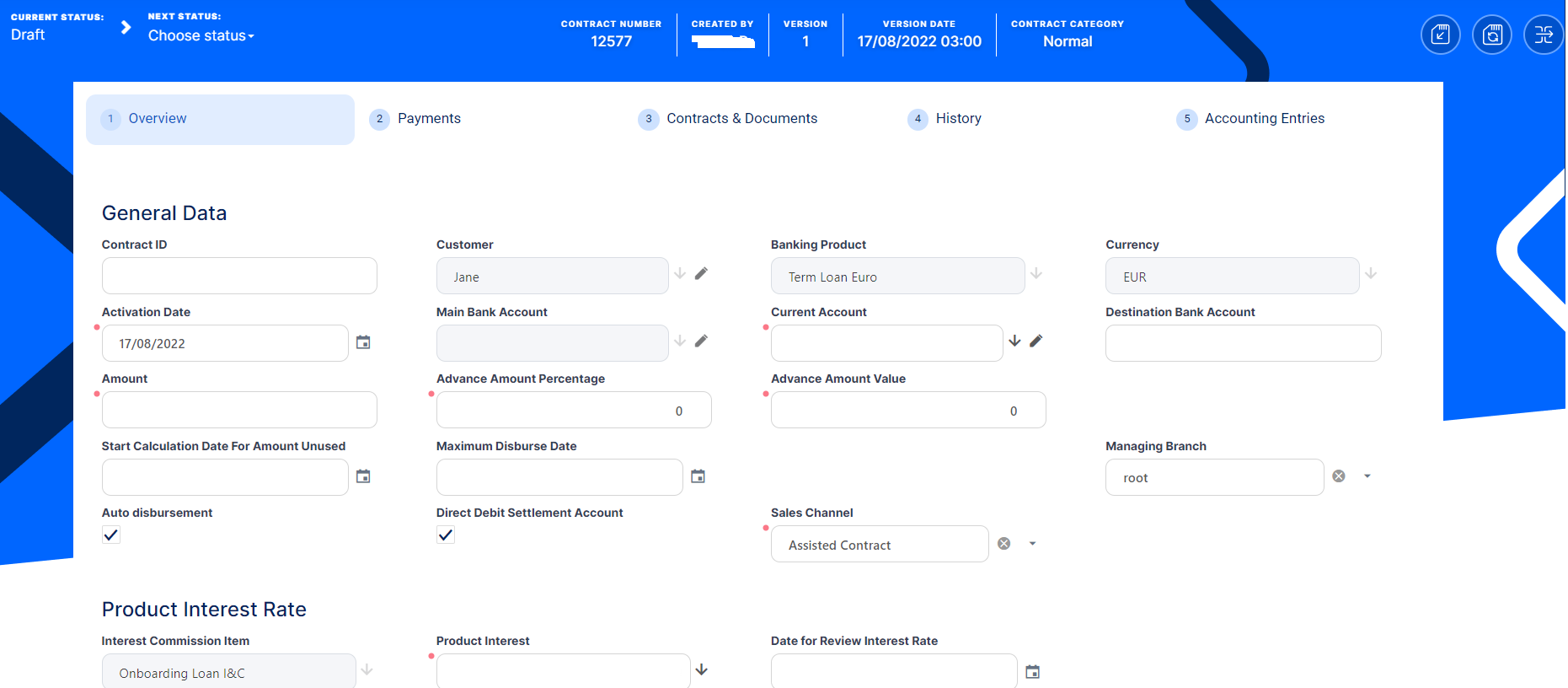

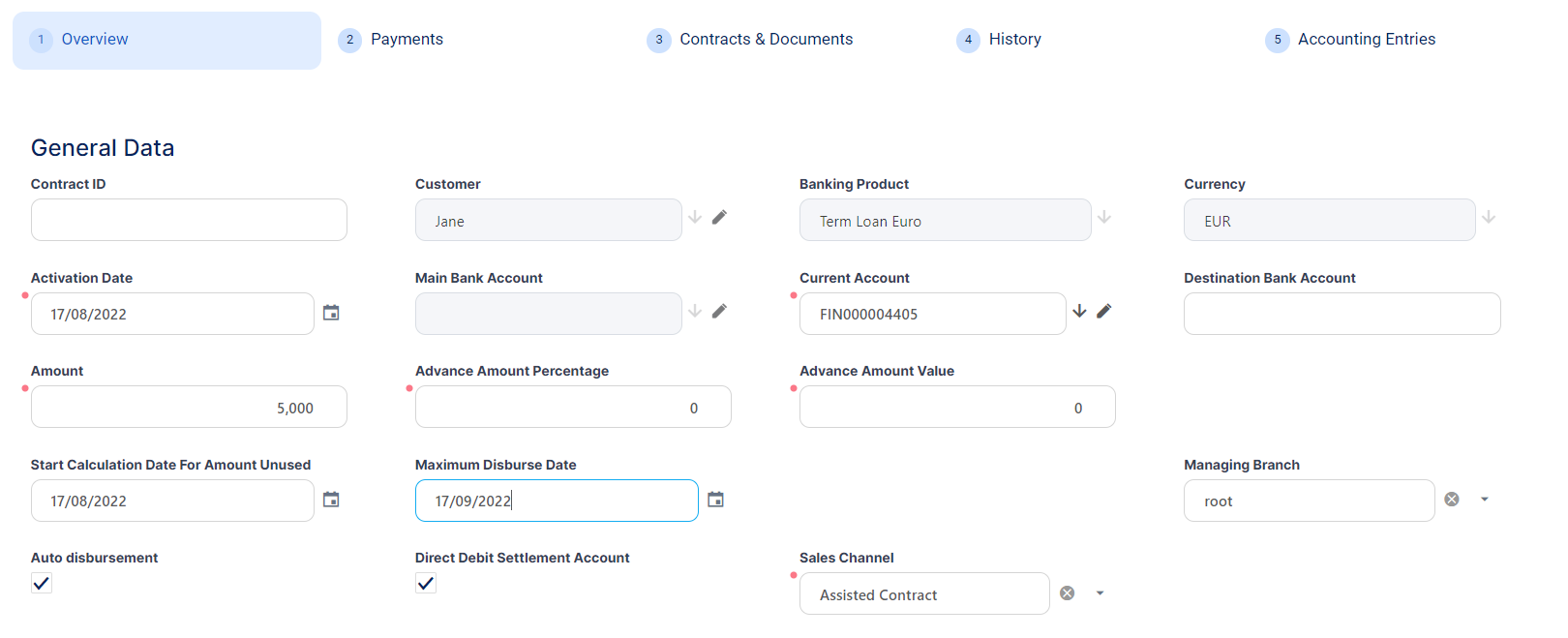

Core Banking saves the contract in Draft status, with minimum default information, such as an auto-generated contract number, created by, version and version number. The previously provided details are kept on screen in the General Data section, but they are no longer available for update. The Currency has been updated from the banking product level.

Proceed to the next steps where the details about the contract are captured and validated against the underlying product, setting the basic elements for the creation of a contract such as customer, banking product, account, interest rate, participants, tranches, fees, and contract covenants, within the newly displayed Overview tab.

-

Fill in or modify the following information:

-

Current Account - Select the current account to be used for settlement.

-

Destination Bank Account - Enter the destination bank account number, an account where the disbursements should be performed, if it's different from the current account selected previously. If the destination bank account belongs to a different customer than the one owning the contract, then any disbursement event happens in that customer's account, and the operation transaction record at the Operational Ledger level mentions the name of that customer in the Destination Partner field. For example, if you input the bank account of a merchant, then the disbursement happens in the merchant's account and the operation transaction record mentions the merchant's name in the Destination Partner field.

-

Amount - Enter the actual amount of credit for the contract.

-

Advance Amount Percentage & Advance Amount Value - Use these in case the product requires a first installment to be claimed on granting the loan itself, or as approval condition - used for orchestrating BNPL where the customer needs to provide a certain amount before benefiting from the loan; requires orchestration of the payment and the approval of such contract should happen only on instruction that payment for advance has been supplied. The 2 fields change one based on the value inserted in the other, so if you insert a percentage the amount is updated based on loan amount.

NOTE Limit validations for contracts with advance amount >0 are performed for Amount - Advance Amount.

When the contract is activated, the available limit amount is decreased with the (Amount - Advance Amount) value.Auto Disbursement = Trueand cannot be changed for contracts with advance amount >0.

If the advance amount is changed back to zero, then the value of theAuto Disbursementcheckbox becomes the default value set at the banking product level and can be edited. -

Sales Channel - Select the channel through which the contract is created.

-

-

Optionally, fill in or modify the following information:

-

Contract ID - Enter a contract ID other than the contract number generated automatically by Core Banking when you saved the contract.

-

Activation Date - Modify the date when the contract is activated. It is automatically completed with the system date.

-

Start Calculation Date For Amount Unused - Enter the date when commitment fee starts being applied. There are instances when, because the loan is granted, the financial institution needs to reserve those funds and make sure they are available when the customer asks for a disbursement, provided all other conditions are met. For such cases, when the financial institution does not generate income from interest, they might want to have a minimum income and thus the commitment fee (commissions with

Commission Unsuagetype). They can also allow for an interval for the amounts to be used and start applying such commissions post that interval. -

Maximum Disburse Date - Select the maximum date by which the loan should be used for the approved contract. It can be that it is required because of internal policies or legislation – such in case of an investment or a mortgage, if you do not use the funds for 6 months, there might be a need for a reassessment. If not selected, this date is calculated based on the

Maximum Period Disburse After Activation (Months)from the banking product level, andMaximum Disburse Date = Maturity Date - 1. -

Managing Branch - This represents the branch of the organization where the contract was created. Suppose you work in a branch or credit center, and you need cases to be linked to a specific location so that you can properly allocate them for further actions. It is automatically completed at contract saving time, but you can select another branch from the list.

-

Auto disbursement - Select this checkbox if the financed amount must be automatically disbursed on the approval of the contract. If selected, Core Banking performs the disbursement transaction immediately after contract approval, and the funds are moved to the settlement account or destination account as per instructions. The auto disbursement property is set at banking product level, but it can be modified at the contract level. The following validations are performed for this checkbox:

- If the contract has multiple tranches, then

Auto disbursement = Falseand it cannot be edited. - If

Auto disbursement = Trueand the contract approval date = activation date, then Core Banking does not generate a new version for the contract. - If

Auto disbursement = Trueand the contract approval date > activation date, then Core Banking generates a new version for the contract.

- If the contract has multiple tranches, then

-

Direct Debit Settlement Account - Select this checkbox if the automated settlement of repayment notifications (the direct debit settlement account) functionality is turned on at the contract level. The value of the checkbox was set at the banking product level, but it can be modified at the contract level. The checkbox can be edited in all the statuses of a contract except

Version Closed,Closed, andCanceled.NOTE TheDirect Debit Settlement Accountsetting at the customer level takes precedence over the setting at the contract level when creating new contracts. For existing contracts, Core Banking applies the setting configured within theCustomerToContractDirectDebitSettlementAccsystem parameter.

-

-

Click the Save and Reload button.

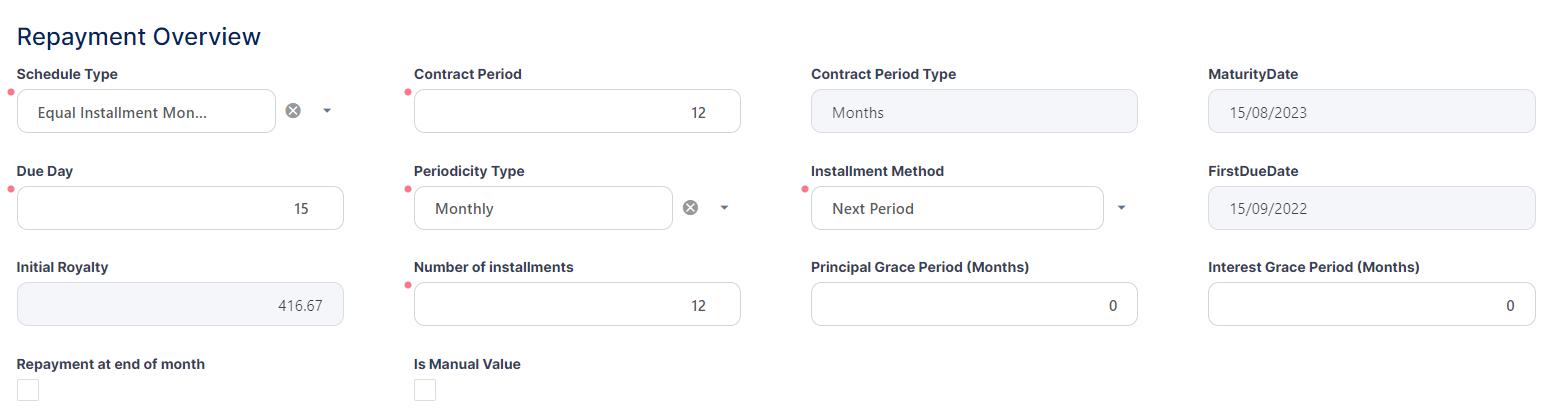

In the Repayment Overview section you should enter term, schedule type and first due date so that Core Banking can properly build the repayment schedule. Optionally you can set a grace period, mention if the due date should always be on the last day of the month and if there is any manual value for the installment.

-

Fill in or modify the following information specific to the contract's repayment schedule:

-

Schedule Type - Select the payment schedule type to be used to calculate the installments of this contract. You can select one of the payment schedule types associated to the underlying banking product in the Details tab > Associated Payment Schedule Types list. Core Banking uses the schedule type to build the repayment plan with equal instalments or liniar payments, include fees on the schedule and arrive to the day basis to be used for interest calculation (30/360).

-

Contract Period - Edit the term of the loan that was automatically completed with the number of contract period of contract period type as it was defined at banking product level, according to your needs. The contract period is used together with Contract Period Type and Periodicity Type. They all need to be in sync and also in sync with the schedule definition itself, and if there are multiple definitions allowed on the product, make sure to pick those working together.

-

Contract Period Type - This field is automatically completed with the contract period type as it was defined at banking product level. You can't edit this value.

-

Maturity Date - This field is automatically completed with the contract maturity date, calculated based on the values of the Contract Period, Contract Period Type, Due Date and Activation Date.

-

Due Day - Enter the exact day of month for installment repayment. If it is set to 31, then the system takes the last day of month. If you manually select the

First Due Date, then this field is automatically completed and not editable. If the periodicity and the repayments are set to every 30 days, Core Banking defaults the due date based on the activation date. -

Periodicity Type - Select the time interval for the repayment schedule. Possible values are set at the banking product level. If the periodicity is set to

Once, then the payment happens one time, at loan maturity. You can only select from periodicity types with the same measurement unit as the selected schedule type's contract period type. For example, if the value in theContract Period TypeisDays, you can only select a periodicity type whose measurement unit is in days. -

Installment Method - Select the installment method to calculate if the first due date is set into the current month or in the next month. Possible values:

-

Actual Period, with the first installment's due date calculated within the same calendar month; -

Next Period, with the first installment's due date calculated within the next calendar month after contract approval.

-

-

First Due Date - Select the date of the first due installment. If you manually select the

Due Day, then this field is automatically completed as calculated based on the information within the Due Date, Periodicity Type and Installment Method, and it is not editable. -

Initial Royalty - This field is automatically completed with the value of an installment. The field is displayed and can be filled in if the selected schedule type is of type

Equal Installment. You can edit this value. If at the selected payment schedule type's level theInstallment Value Customfield isFalse, then theInitial Royaltyfield at the contract level is read only. -

Initial Principal Value - This field is automatically completed with the value of the principal within an installment. The field is displayed and can be filled in if the selected schedule type is of type

Equal Principal. You can edit this value. If at the selected payment schedule type's level theInstallment Value Customfield isFalse, then theInitial Principal Valuefield at the contract level is read only. -

Number of installments - This field is automatically completed with the number of installments to be paid for this contract, calculated based on previously defined values.

-

Principal Grace Period (Months) - This field is displayed only if the banking product allows a principal grace period. Enter a value in months for the grace period allowed for principal repayment for this contract. The value inserted in this field should be between the minimum and maximum grace period set at the banking product level.

-

Interest Grace Period (Months) - This field is displayed only if the banking product allows an interest grace period. Enter a value in months for the grace period allowed for interest repayment for this contract. The value inserted in this field should be between minimum and maximum grace period set at the banking product level.

-

Repayment at end of month - If you select this checkbox, then the due day of the contract is automatically set to the last day of the month, and the repayment schedule is calculated with an installment in the last day of month.

-

Is Manual Value - If you select this checkbox, then you can manually enter the value for royalty or principal, thus overriding the values automatically calculated by Core Banking.

-

If

Is Manual Value = False, then theInitial Royaltyand theInitial Principal Valuefields are read-onlyand cannot be modified. -

If at the selected payment schedule type's level the

Installment Value Customfield isFalse, then theIs Manual Valuefield at the contract level is read only. -

If

Installment Value Custom = True, then theIs Manual Valuefield at the contract level is editable, withFalsedefault value.

-

-

-

Click the Save and Reload button.

Enter the details about the Product Interest Rate applied to the loan. Depending on the product definition again, you have a list of interest definitions that you can bring along to the contract.

To manage the product interest rate as it must be applied to this contract:

-

Fill in or modify the following fields:

-

Interest Commission Item - This field is automatically completed with the interest & commission item defined at the product level, if only one item is found at the product level. If the selected product has more items, you must select one from the list.

-

Product Interest - Select from the interest to be applied for this contract. Only the interests associated to the selected banking product are displayed within the list. Penalty interests cannot be selected here.

-

Date for Review Interest Rate - Enter the date for reviewing the interest rate applicable for the remaining amount. This date must be between

Activation DateandMaturity Date, otherwise, an error is displayed.

For variable interest, this field is automatically completed with theReference Rate Date+Reference Interest Periodof the underlying interest definition, from the base type interest attached to variable interest. You can edit this field. For months where the date is over lapsed, the last day of the month is used for the calculation (for example, if you specify 30, then in February the system takes the last day, which can be the 28th or the 29th).

-

If the underlying interest definition has referenced a variable interest rate, the details included other fields for you to complete:

-

Margin – The margin applicable on top of the variable interest rate.

-

Reference Rate Date – The date to be considered in order to arrive to the applicable rate for the underlying variable interest (EURIBOR as of 30th June 2022).

-

Reference Rate – The underlying rate for the variable interest as captured in Core Banking for the date above.

-

Click the Save and Reload button.

Fill in any other mandatory fields from the General Data and Repayment Overview sections, otherwise you can't successfully save the contract.

Define the information about the contract interest rate (or rates, if you selected a Collection type interest rate in the previous Product Interest Rate section) in a table format, in the section Contract Interest Rate section, which appears only after saving the selected product interest rates.

You can edit the tables cells, so you can customize the interest rates selected at the product level, if the interest and commission list was defined as negotiable, to obtain the desired interest rates configuration at the contract level. You can also add or delete interest rates, using the Add Interest Rate,

The information disappears if you change the product interest, tenor, first due date, maturity date, contract period, or activation date. In this case, save the contract again to display the updated information.

To customize the information specific to each of the contract's interest rates:

-

In the Contract Interest Rate section, edit the existing information that was automatically completed based on your product interest rate selections:

-

Interest - Automatically completed with the interest (or interests, for

Collectiontype product interest rate) selected in the previous Product Interest Rate section. You can select from the drop-down list the interest to be applied for this contract. Only the interests associated to the selected banking product are displayed within the list. Penalty and overdraft interests cannot be selected here. Depending on the selected interest, other fields can be displayed to be filled in. -

Start Date - The interest's start date, automatically completed with the contract's activation date.

-

End Date - The interest's end date, automatically completed with the contract's maturity date.

-

From Installment - The first installment for which this interest is applied to the contract.

-

To Installment - The last installment for which this interest is applied to the contract.

-

Minimum Interest Rate - This read-only cell is automatically completed with the minimum interest rate applicable for the contract, defined at the banking product level.

-

Fixed Rate - The fixed rate of the interest. You can only change it if the interest at the banking product level was marked as

Is Negociable. -

Margin - This cell is automatically completed with the margin of the previously selected product interest. You can only change it if the interest at the banking product level was marked as

Is Negociable. If the product interest was not selected, you can manually enter the margin. -

Reference Rate - This read-only cell is automatically completed with the interest type's definition's reference rate valid at the previously selected date.

-

Total Interest Rate - This read-only cell is automatically completed with the calculated total interest rate of the previously selected product interest and any values entered for margin and reference rate. If the product interest was not selected or if the interest at the banking product level was marked as

Is Negociable, you can manually enter the interest rate. -

Notified - This is a read-only checkbox. For contracts in

Version Draftstatus, it shows you whether the installments range shown on this table line was already notified or not. -

Past Unnotified - This is read-only cell read-only checkbox. For contracts in

Version Draftstatus, it shows whether there are days that already passed from the current month's not yet notified installment, days for which you can't change the interest rate.

-

After performing the desired changes, make sure that the interest rate(s) cover the entire tenor of the contract, from activation date until maturity date, and there are no overlapping intervals, otherwise an error prevents you from approving the contract.

-

Click the Save and Reload button.

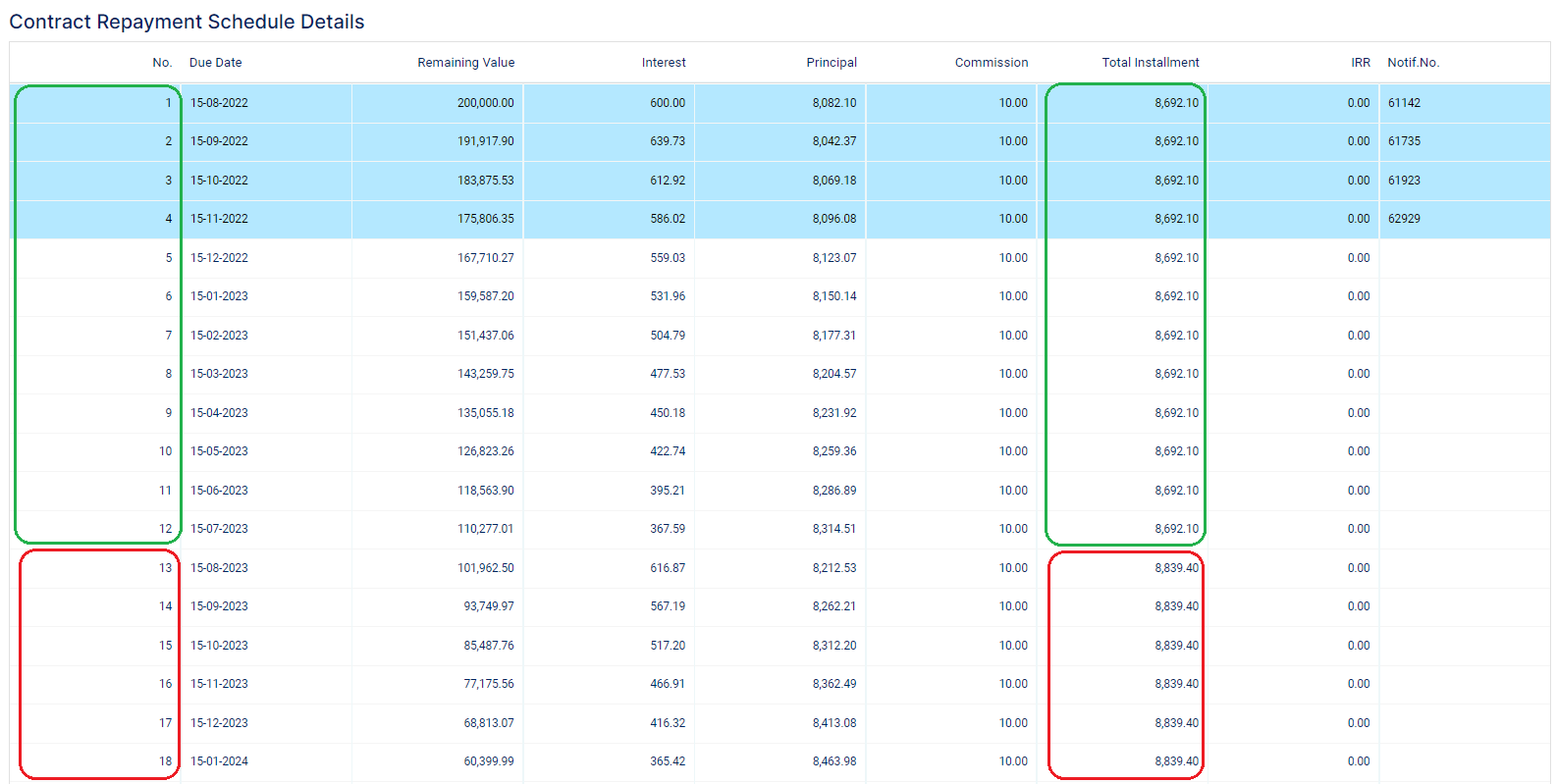

Later, after contract approval, the contract repayment schedule is calculated taking into consideration the contract interest rates as defined in this section. For example, for a multiple interest rates, the installment amounts differ depending on the interest rate applicable for those installment numbers. The picture below shows different values calculated for the repayment schedule of a loan with multiple interest rates, where an interest rate was applied for the first 12 installments, and another interest rate was applied for the rest of the installments.

To customize the information specific to each of the contract's penalty interest rates:

-

In the Contract Penalty Interest Rate section, edit the existing information that was automatically completed based on your product interest rate selections:

-

Interest Name - Automatically completed with the penalty interests selected in the previous Product Interest Rate section. Only the penalty interests associated to the selected banking product are displayed within the list.

-

Start Date and End Date - The penalty interest's start and end dates, automatically completed with the contract's activation, respectively maturity date.

-

Fixed Rate - The fixed rate of the penalty interest. You can only change it if the interest at the banking product level was marked as

Is Negociable. -

Margin - This cell is automatically completed with the margin of the previously selected product interest. You can only change it if the interest at the banking product level was defined as variable and marked as

Is Negociable. -

Reference Rate - This read-only cell is automatically completed with the interest type's definition's reference rate valid at the previously selected date.

-

Total Interest Rate - This read-only cell is automatically completed with the calculated total penalty interest rate as Fixed Rate or Margin + Reference Rate.

-

Operation Item - The contract's operation item to which the penalty interest is applied.

-

After performing the desired changes, make sure that the penalty interest rate(s) cover the full contract period, from activation date until maturity date, and there are no overlapping intervals, otherwise an error prevents you from approving the contract.

-

Click the Save and Reload button.

Later, after contract approval, you can change the penalty interest rate by versioning the contract and editing the information in this section. Thus, the new penalty rate becomes effective after approving the contract version, only impacting future calculations and notifications.

If allowed from the product definition, you can amend the closure settings of the contract, the way Core Banking should behave once the loan is repaid and the contract can be closed. Most of the times this is not something that you have to access, but it adds extra flexibility at the contract level. This may prove useful if you suspect there may be reasons to keep a contract open for some time post recovering all amounts for instances when there may appear claims of funds (SEPA DD) or other similar cases.

The Closure Settings section is only displayed for contracts based on banking products having the Closing Is Flexible = True setting.

To amend the closure settings brought from product level here at the contract level:

-

Fill in or modify the following fields:

-

Automatic Closure – If selected, Core Banking automatically closes the contract once all other conditions are met. This field is automatically completed with the value defined at the banking product level, but you can modify it.

-

Select this checkbox to instruct Core Banking to close the contract automatically when the available amount becomes zero and there are no further amounts to be recovered, and after the number of days set as buffer before closure pass and

Closure Date = Current Date. -

Deselect it to instruct Core Banking to keep the contract open, regardless of the fulfillment of its maturity and balance criteria, waiting to be manually closed by changing its status to

Closed.NOTE

Revolving loans are closed only after maturity. In this case, the available loan amount is considered as balance.

You can perform contracts events as specified in the Allowed Transactions section of the banking product, plus manual closure while the contract is pending closure. Performing any other transactions displays an error message.

-

-

Real Time Closure – If you select this checkbox, when the amounts become zero and the loan is not a revolving one, the contract is closed automatically. If

Real Time Closure = True, thenBuffer Close Days = 0andAutomatic Closure = True. For more details about the real-time closure, see Close Contracts RealTime(CB) Job. -

Buffer Close Days - Enter the number of days used as buffer before automatically closing the contract. If

Buffer Close Days > 0, thenReal Time Closure = False. Core Banking waits the entered number of days after the contract's balances reach zero, and at the end of that day the contract is closed. -

Balance Off Date – This is a system maintained field and it is populated with the date on top of which Core Banking adds the Buffer Close Days to arrive to the Closure Date.

-

Closure Date – This is a system maintained field and holds the date when the contract is closed. For automatic closure, the date is calculated by Core Banking as Balance Off Date + Buffer Close Days.

-

-

Click the Save and Reload button.

Once you defined the mandatory details, then saved and reloaded the contract, Core Banking updates some of the next sections on the page, based on product definitions:

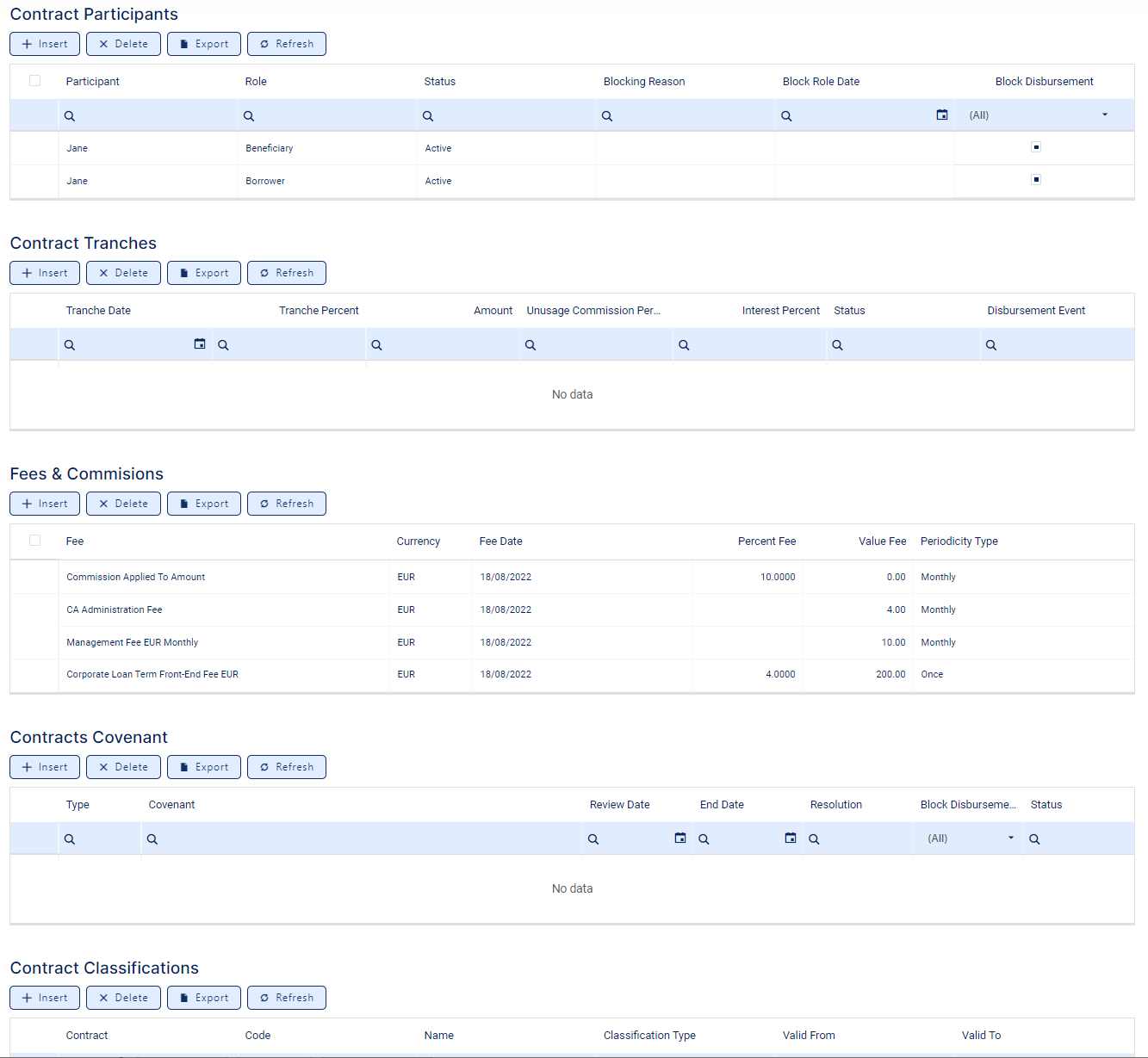

Core Banking brings the Contract Participants, the Borrower being also Beneficiary of the funds and the Customer who is granted the loan. If needed, you can add other participants to the contract, like Guarantors, Co-Debtors, etc. There may be cases when some roles are mandatory for a product. Those are detailed in a separate section. If there is a mandatory role defined in the banking product definition, Core Banking displays an error on trying to approve the contract.

Contract Tranches is a section where you can implement progressive access to the funds. This is valuable in case of loans granted for investment projects where you can know upfront that there is a plan for the project and payments need to happen for each stage of the project, those stages being known from the start.

Another important section brought from the product definition is the Fees & Commissions. Depending on the system setup, you are allowed or not to amend fees and commissions in this section.

Contract Covenants section displays the covenants that applicants must abide by after getting the loan, configured at the product level. Such conventions are usually applicable for corporate clients that must meet certain requirements in order to continue to receive disbursements and not only: submit balance sheet every x months, have account turnover of at least x percent from average monthly turnover, provide other relevant documents from authorities. In this section, you can manage covenants for the contract. These covenants would need to be monitored procedurally; Core Banking doesn't have the logic in place to implement automated processes.

You can use the Contract Classifications section to capture various classifications that might be relevant for the financial institution for that loan at a moment in time. It is a placeholder for such details and there is no automated logic in place to update them. In implementation this can be used for other developments if required.

After defining the relevant details of the contract, proceed to contract approval.