Life and Health

The Life and Health module allows the user to gather the necessary information, and set a quote for when the customer applies for an insurance.

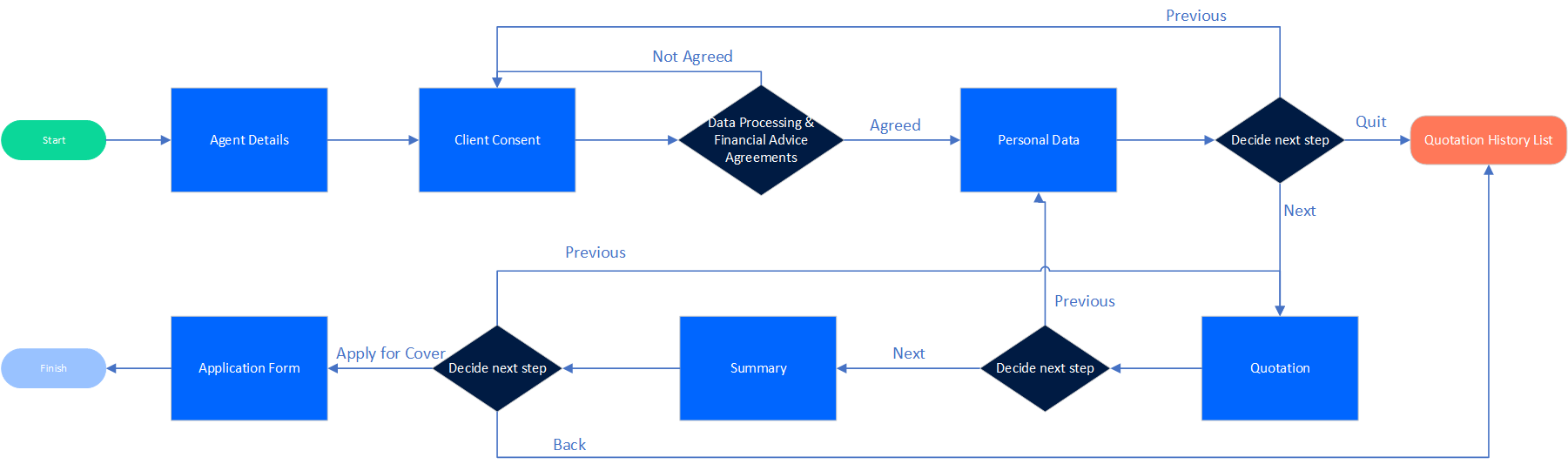

The module allows gathering more than just the basic information about the customer in order to establish a quote. Hence, a financial needs analysis, or a Demands and Needs Test (DNT) stage is introduced for the customer to determine the best fitting package that they can apply for. The customer can then select one or more of the packages from a list of automatically generated quotations based on the personal and financial information previously provided. The customer can then apply for a term insurance policy.

The quotation flow is presented in the diagram below.

The premium is automatically calculated based on the customer's age and the selected term.

The following insurance lines of business are included:

-

Term life with multiple riders;

-

Permanent health insurance;

-

Health insurance, including core and ancillary benefits.

The Life and Health solution offers the user the ability to apply for a new life quote and view the existing life quote records.

Industry Business Processes

FNA (DNT) Financial Needs Analysis: In order to make an offer that is suitable to the client's insurance demands and needs, a questionnaire is provided in order to gather information such as:

-

Personal details relating to all family members and dependents.

-

Details of income and sources of income, such as earnings from employment, investments, pensions and other types, from all contributing family members.

-

Details of any investments that are not currently generating income.

-

Other assets, for example a residential or commercial property.

-

Liabilities, such as

-

Loans and/or mortgages.

-

School fees.

-

-

Outgoings, such as

-

Loans, credit cards and mortgages

-

School fees

-

Existing life, pensions, health and general insurances

-

Property maintenance, such as council tax, water rates, utilities

-

Groceries, clothing, medical

-

Holidays and pastimes.

-

-

Existing personal insurance benefit levels - life, health and pensions.

-

Existing employee benefit levels -life, health and pensions.

This data is used to determine the financial shortfalls that would be realized on death, permanent or temporary disability of one or more of the contributing family income contributors. Based on the customer's answer on the DNT, the system is able to generate an illustration or quotation of the premium levels required to provide those benefits.

Illustration / Quotation: This process is initiated on receipt of a request for a product quotation. Either a direct request or driven from the FNA/DNT process, typically this involves just the minimum information from the individual or group of individuals, necessary to enable the relevant calculations to be performed and the results returned for formatting into the quotation to be produced. The ability to enable the collection of a broader set of the prospective insureds information is supported, such as:

• Height/weight;

• Occupation (Class);

• Nicotine usage;

• Possibly others such as alcohol use;

These requirements may vary from insurer.

The quotation results are stored until such time as they are selected for progression to an application, or can be deleted or otherwise archived in accordance with the offices business practice and applicable regulation, e.g. GDPR.

Apply (New Business Process): The identification of an application activates the New Business process. The application is checked for errors and omissions, and the user can make corrections. If the responses to the health questionnaire indicates the need for further underwriting, then the application data is referred for medical underwriting. This may need to be passed to an external underwriting system. The main New Business Process continues as far as possible before completion of underwriting and/or rectification of any errors or omission prevents any further processing.

Not Proceed With: The NPW process deals with the cancellation of the application before issuing the policy. This can be initiated automatically or manually. The automatic process is triggered from the New Business or Underwriting when the requests for underwriting evidence or additional application details have not been responded to within the agreed time lines. Users, including authorized representatives can manually initiate the NPW processes.

Not Taken Up: The NTU process deals with the cancellation of an application after policy issue but while the application is active during the cooling off period.

Port Issue Monitoring: This process runs in the background, checking for the completion of the cooling off period. The contract then changes in order to confirm the completion. In the duration of this period, the requests for an NTU can be processed.