Credit Facilities

A credit facility is a grouping of multiple credit products that a client has arranged with a bank under a single credit limit. Banks can offer companies a credit limit for the company as a whole, and the company can then take on different loan products without the need for separate risk assessments. This simplifies access to funds for companies and greatly reduces time-to-cash. Credit facilities also create operational efficiencies for the bank, because individual loans no longer need separate risk assessments.

FintechOS Core Banking allows banks to create credit facility agreements for their customers based on approvals.

Credit facility management is available via the Core Banking Corporate 3.0 package, which has to be installed on top of the Core Banking 3.0 package.

Business Logic

Let's say a bank approves a credit facility for a group or a customer up to EUR 100.000, to be used by the credit facility participants among various currencies:

-

guarantees allowed in EUR and USD;

-

term loans allowed in EUR and GBP;

-

overdrafts allowed in EUR.

First, an agreement is made between a bank and a customer (total exposure limit). This limit will be used while creating the credit facility, making sure that the credit facility limit amount does not exceed the total exposure limit of the customer. The approval can be revolving or non-revolving, thus both limit and facility have the same nature.

The credit facility holds details about:

-

Allowed banking products, with their preset currency

-

Allowed customers, if the facility is granted for a specific group of customers

-

Covenants, if needed

-

Prices:

-

Unutilized fee, as a percentage to be applied to daily unused amount. The fee is collected from current/ servicing account with a given frequency/ periodicity.

-

Interest and commission related elements, for negotiable product costs.

-

Loan contracts are entered whenever the customer asks for disbursements, according to the credit facility setup.

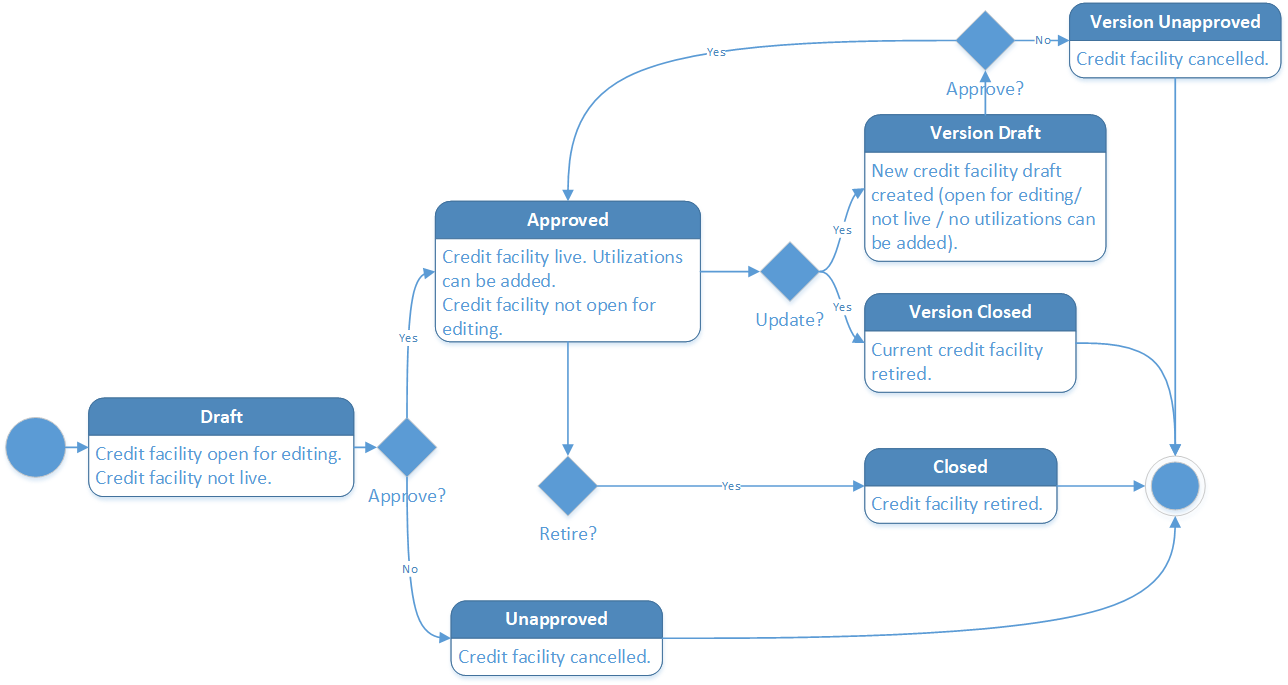

Credit Facility Statuses

Credit facilities are complex agreements between a bank and its customers. Therefore the four eyes principle is applicable here, meaning that a record should be approved by a second bank employee, with higher authorization rights.

A credit facility record has the following business workflow statuses:

-

Draft - the status of a newly created credit facility record that was not yet sent for approval. While in this status, you can edit the fields from the record's Credit Facility tab, but you can't add utilizations to it. Send the record to approval after editing all the necessary details.

-

Pending - this is a system status applied to credit facilities sent for approval, but not yet approved. No updates are available in this system status.

-

Approved - the status of a credit facility record after being authorized by a user with credit facility approval competencies. While in this status, you cannot edit the record's details, but you can add utilizations to it within the Credit Facility Utilizations tab. If you need to alter the credit facility's details, create a new version based on the current credit facility.

NOTE

Each facility utilization must also be approved by a user with credit facility utilization approval competencies, otherwise, the disbursement of the utilization will not be performed by the system. -

Closed - the last status of a credit facility, after manually closing it or after creating a new version based on the current version. No updates are allowed on the record.

In order to use the credit facility, it must be in the Approved status.

Credit Facility Life Cycle

First, an agreement is made between a bank and a customer - usually, a legal entity, for the customer to have easy access to funds whenever in whichever banking product they need it. The amount cannot exceed the customer's approved Total Exposure type limit.

This agreement is recorded in the bank's system by a clerk, in the form of a credit facility. All details of the agreement are captured while creating the credit facility record: who are the participants with access to funding, what's the usable amount in the chosen currency, what products can be used within this agreement, when is the agreement applicable, under which conditions, whether the facility's amount increases or decreases over time and so on. The clerk fills in all the mandatory details, saves the record still in Draft status, and then sends it for approval.

Another employee of the bank, with higher authorization rights and with credit facility competencies, consults the record and approves or rejects the credit facility, depending on the details entered before by the creator of the record. If rejected, the credit facility's status becomes Closed.

If approved, the credit facility, now in Approved status, can be used by the customer to access funds. Its details cannot be altered anymore, but the clerk can add utilizations to it up until the credit facility's maturity date, in the form of contracts for banking products listed in the credit facility.

These utilizations, being in fact banking contracts, after creation are still in Draft status, and thus have to be further approved by a second employee of the bank, with corresponding contract approval rights. After being approved, a utilization disburses its amount in the customer's account. This amount is taken from the credit facility, thus the available amount is lowered with the sum of the approved utilization.

The total amount of approved utilizations, in any of the banking products' currencies, cannot exceed the amount approved in the credit facility, calculated in the facility's currency based on the exchange rate valid on each day.

Fee values and accruals are calculated for the approved utilizations and displayed in the Credit Facility Utilizations tab, along with any repayment notifications.

Credit facilities can be manually closed if needed. Records in Closed status cannot be altered in any way.

If the details of an approved credit facility have to be updated, then a new version of the record must be created. The new version of the record is created in Draft status, thus restarting the life cycle.

Changing Credit Facility Statuses

You can manage a credit facility's life cycle by changing its status from the top right corner of the screen.

The credit facility status transitions are illustrated below:

Note that:

- Once a record is live, its settings can no longer be modified.

- If you want to update the details of a live credit facility, you must create a new credit facility version.

- When you create a new credit facility version, the current version is retired; no updates are allowed on the retired version.

- Every credit facility version starts in a draft state and must go through an approval process before going live.

- Only one version of a credit facility can be live at one time.

As a best practice, new records or new versions of existing records created on a specific day should be approved on the same day.

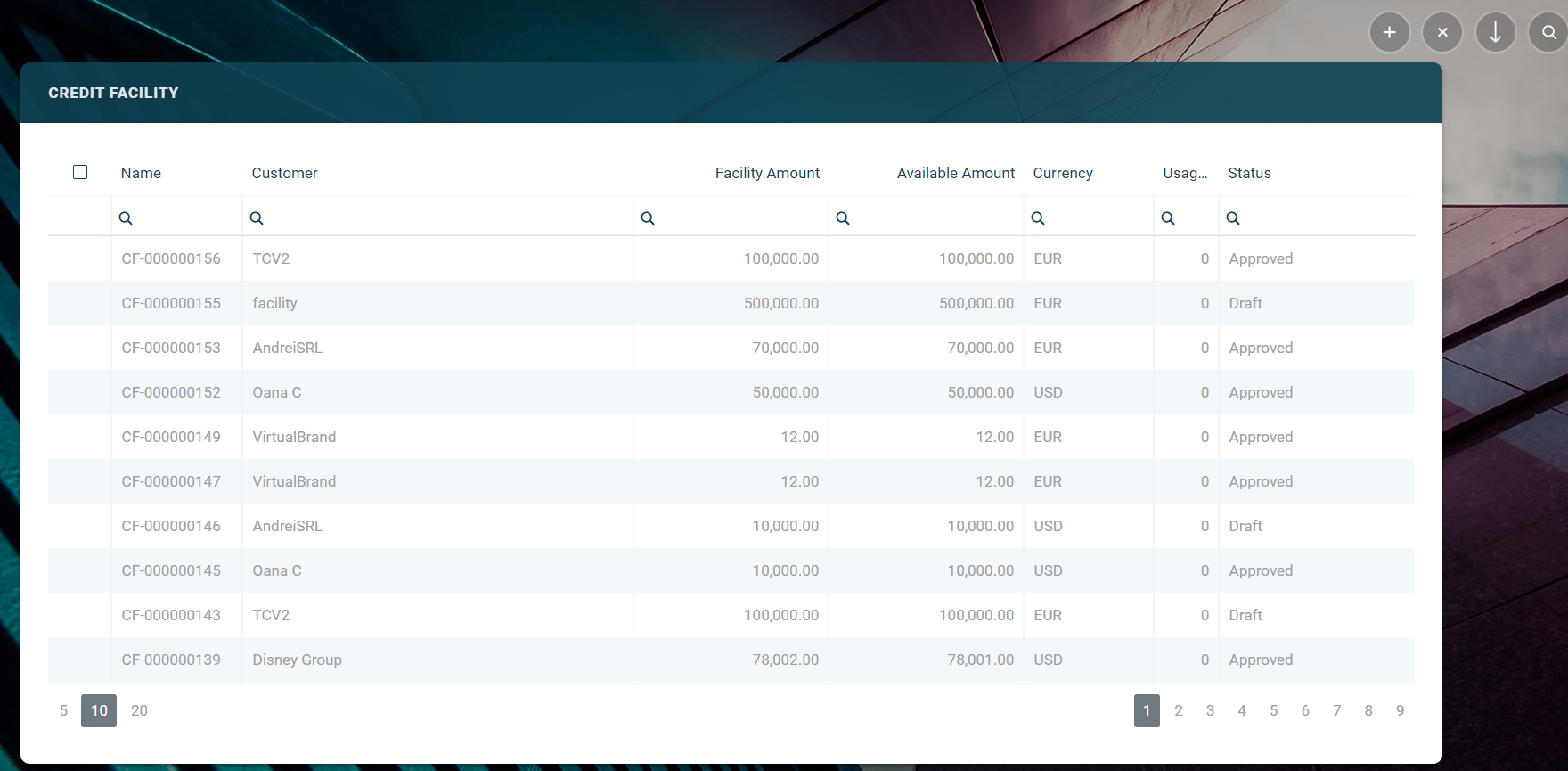

Managing Credit Facilities

To manage credit facilities:

-

Log into FintechOS Portal.

-

Click the main menu icon at the top left corner.

-

In the main menu, expand the Core Banking Operational menu.

-

Click Credit Facility menu item to open the Credit Facility page.

In the Credit Facility page, you can:

-

Create a new credit facility by clicking the Insert button at the top right corner.

-

Edit a credit facility from the list by double-clicking it.

-

Delete a credit facility by selecting it and clicking the Delete button at the top right corner

-

Search for a specific record by filling in any or all the column headers of the displayed credit facility records list.